Subscriber note: Cash Equivalence is currently operating as an ad hoc operation due to the funding and independence constraints of the author. However, the objective is to become a daily and independent service as soon as it is tenable to do so. For now, we’ve decided the best way to keep the output consistent while growing our revenues is not to over-promise and under-deliver. As a result, the daily peg is temporarily turning into the weekly peg and innovative analysis will be published as and when.

But fear not, in the interim, our expertise — and identity — will be available to paid subscribers on a bilateral and private basis. Just drop us a note.

For more contemporaneous links see our Twitter account

If you’re interested in backing or investing us, please contact us via this portal or DM us on the above X account.

Industry News

— Tether has decided not to freeze USDT smart contracts on legacy networks such as Omni Layer, Bitcoin Cash SLP, JUsama, EOS and Algorand.

Key graf: “While users will still be able to transfer the tokens between wallets, Tether will discontinue direct issuance and redemption on these blockchains. This means the tokens will no longer be officially supported as other Tether tokens.”

— CoinDesk reports that Aave Labs has launched a new platform dedicated to institutional borrowers to access stablecoins using tokenized versions of real-world assets (RWAs) like U.S. Treasuries as collateral.

— Decrypt reports that Stablecoin-backed card company Rain, which partnered with Visa this year, has raised $58 million as part of a series B funding round.

— Decrypt reports Switzerland-based stablecoin platform M0 raised $40 million in Series B funding, as it seeks to shake up the relationship between token issuers and blockchain developers, according to a press release on Thursday.

Analyst reports:

— Rabobank’s deep dive on stablecoins: $tablecoins in an un$table $ystem

Key grafs: “Moreover, the US could lean on Saudi Arabia, the UAE, and Qatar --the source of much of Europe’s LNG, for example – to insist on payment for their energy in USD stablecoins: that would mean everyone who buys energy – except those who buy from the likes of Russia or Iran, etc. – needing to hold them.”

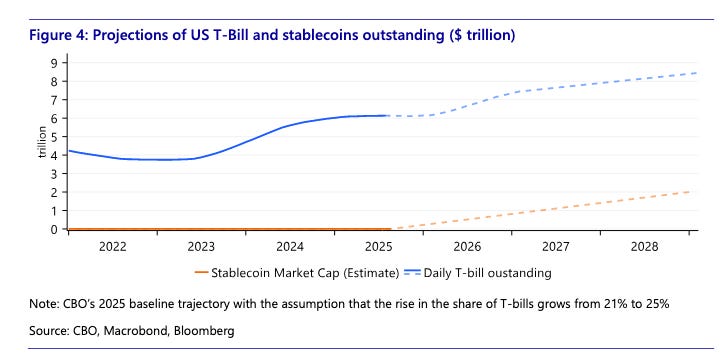

Key chart: “In theory, this implies the need for an ever-growing amount of T-Bills for the US to allow USD stablecoin-based trade to expand, just as with the current Eurodollar system – the ‘Triffin Dilemma’. Failing that, they could become akin to a deflationary gold standard (and/or trade access to the US is necessarily de facto limited).

However, USD stablecoins can also be backed by USD repo, reverse repo, or bank reserves (even if the broader the range of assets involved the greater the potential risks of worrying financial instability become over time). That could be one solution. Yet the US doesn’t want to repeat past Triffin errors which it sees as having helped deindustrialise it: as such, hypothetically, USD stablecoins may gradually allow a separate ‘track’ to the broader fiat Eurodollar market just for trade. If so, any Triffin ‘bottlenecks’ may therefore be deliberate”

— The new currency war: The US-China digital rivalry as a test of monetary discipline (CEPR) (paper by Eduardo Levy Yeyati and Sebastian Katz). It’s all about the paradox at the heart of stablecoins they say!

Key graf: “While pushing the e-CNY central bank digital currency, China has opened the door to yuan-pegged private stablecoins from firms like JD.com and Ant Group. Officials worry that without competitive yuan stablecoins, cross-border payments will remain dominated by dollar stablecoins — a ‘strategic risk’ in the words of former Bank of China Vice President Wang Yongli.

This dual strategy — centralised central bank digital currency plus private stablecoins — recreates the currency board dilemma. To grow, private yuan stablecoins will face the same temptation toward intermediation and leverage as their dollar counterparts, potentially undermining their own stability and, by extension, monetary control.”

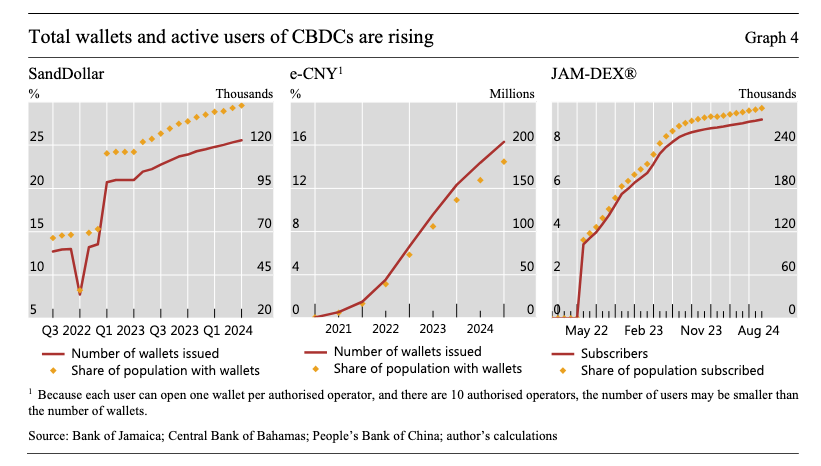

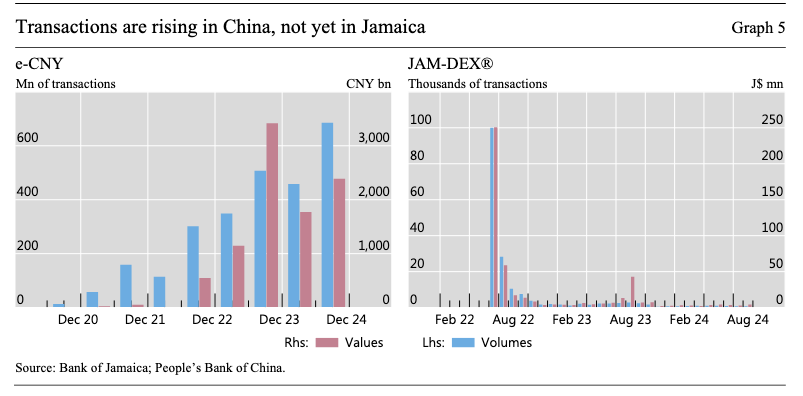

— SSRN publishes: Retail CBDCs In Practice: The Experience of the Sanddollar, E-CNY and JAM-DEX®

Key graf: “Lack of awareness of CBDC initiatives, misinformation and lack of trust can each be very damaging to the success of a CBDC project. Central banks have adopted different strategies to generate awareness about their CBDC projects and to communicate about key features and answer questions. For example, the CBOB ambassadors programme, operated by the Adoption Unit, deploys persons into the field to educate businesses and consumers on the SandDollar, and to assist them with starting the onboarding process. This hands-on assistance has helped to engage more users, both from a business perspective and a consumer perspective.”

Key chart:

Central Banks

— The ECB’s Foreign exchange contact group talked stablecoins in June.

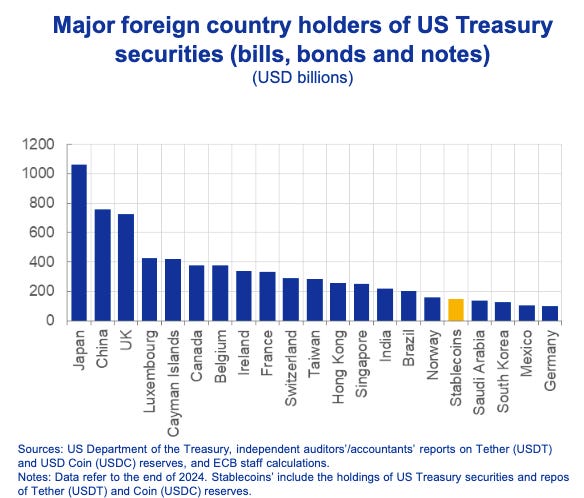

Key grafs: “The recent development in stablecoins could materially impact demand for US dollar and US denominated securities. The adoption of DLT-based financial products seems to be reaching an inflection point, supported by regulations like the US Genius Act, which could accelerate a shift away from traditional fiat systems. Members mentioned some large US retailers considering setting up their own stablecoins. They highlighted risks for regulatory arbitrage and raised concerns about the vulnerabilities of stablecoins to US Treasury market risks, and vice versa."

Key chart:

— ECB’s Philip Lane explains to the IMF’s Finance and Development magazine “Why Europe needs a digital euro”.

— Hélène Rey, Lord Raj Bagri Professor of Economics at the London Business School, dives deep into stablecoins in the same publication.

Key grafs: “If the use of US dollar stablecoins increases mas- sively worldwide, it could hollow out banking sectors because of competition for deposits. If banks themselves issue stablecoins, it could curb lending and increase US Treasury holdings—assuming these are the main assets backing the stablecoins — on the asset side of the balance sheet, a development akin to narrow banking. The effects on systemic risk, as well as the potential questionability of some actors’backing of stablecoins and the ensuing run risks, bear a close look. And the classic cost of dollarization around the world should be kept in mind: It can alter the transmission channels of monetary policy and hinder macroeconomic stabilization.”

“For the rest of the world, including Europe, wide adoption of US dollar stablecoins for payment purposes would be equivalent to the privatization of seigniorage by global actors.”

— Stablecoins were a big discussion point for the FOMC this month. (CryptoSlate) Minutes available here.

Key graf: “Many participants discussed recent and prospective developments related to payment stablecoins and possible implications for the financial system. These participants noted that use of payment stablecoins might grow following the recent passage of the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act). They remarked that payment stablecoins could help improve the efficiency of the payment system. They also observed that such stablecoins could increase the demand for the assets needed to back them, including Treasury securities. In addition, participants who commented raised concerns that stablecoins could have broader implications for the banking and financial systems as well as monetary policy implementation, and thus warranted close attention, including monitoring of the various assets used to back stablecoins”

— Current and former PBoC heads disagree on stablecoin hype (Central Banking) (SCMP)

Key graf: “Although many believe stablecoins will reshape the payments system, in reality, there is little room to cut costs in the current system, particularly in retail payments,” he added.

Podcasts

— Rabobank’s Michael Every on 4D Chess: Dollarizing the World by the Back Door I Michael Every

— Financial Sense interviews Izabella Kaminska.

New players

— Plasma is a high-performance layer 1 blockchain purpose-built for stablecoins. Backed by Founders Fund, hiFramework and Bitfinex. It’s been active since October 2024.

USP? It aims to allow zero-fee USDT transactions.

Why does that matter? Moving USDTs currently isn’t as easy as you’d think. If you want true security you need to pay volatile gas fees and hold ether accounts. And if you want cheap transactions you need to reduce yourself to more centralized rails like Tron.

How serious is the operation? Plasma raised $20 million in a Series A fundraising by Framework Ventures in February, 2025. This follows a $4 million seed round from early investors, the creme-de-la-creme of the space, Peter Thiel, Paolo Ardoino and Bitfinex.

Who’s who? The founder is Paul Faecks, a serial enterpreneur based in Berlin. He’s a graduate from the Technical University of Munich.

In his own words.

Highlights: Faecks also explains Plasma's aim is to offer gasless USDT transfers by utilizing a custom consensus mechanism (whatever that is) and Bitcoin security, contrasting it with the limitations of existing solutions like Ethereum and Tron.

He admits, however, that preventing spam in a gasless environment will be complex.

How will it make money? He’s vague, but hints it will replicate the same business model that all blockchains use. That suggests via a native token.

Liquidity incentives are already coming (otherwise known as ‘inducements’). The Block reported users can gain Plasma exposure via a Binance Earn product that pays daily USDT yield plus an XPL airdrop allocation ahead of the token generation event. It’s called a “Plasma USDT Locked Product”.

In plain english, that means users get free transactions but are incentivised to keep their cash as stagnant as possible via “air drops” (aka interest rewards).

Cash Equivalence view: Creating a rail system that absorbs the fees isn’t a bad idea. One of the remaining frictions for mass uptake is the complexity of the eco-system, with normies regularly bewildered by how to actually transfer money across chains, without encountering KYC frictions for every cross-chain hop. Absorbing fees might seem bananas, but there is a precedent in the U.K. banking system that has famously offered free bank accounts in a bid to cross-sell other more profitable products like mortgages to customers once they’re trapped within their ecosystems.

The risk factor is that regulators have spend decades trying to break banks out of these bad habits. The Open banking systems they’ve forced upon the sector are a much better deal for users as a result. If you end up trapped in a particular ecosystem because it’s too expensive to leave, you become the product — and that in theory is the antithesis of the crypto spirit.

— MetaMask enters stablecoin scene with $mUSD launch on Ethereum and Linea.

Resources

— A strategic guide for fintechs and builders exploring stablecoins (From Dynamic.XYX)

Who’s who in stablecoins?

We’re keeping track of emerging experts and players in the field. Today we’re spotlighting Tommaso Mancini-Griffoli

Who’s he? Deputy Division Chief, Monetary and Capital Markets Department at International Monetary Fund

What does he look like? Beardy authoritative-looking chap, with an american-european

Does he know what he’s talking about?

From his bio: “Prior to joining the IMF, Mr. Mancini-Griffoli was a senior economist in the Research and Monetary Policy Division of the Swiss National Bank, where he advised the Board on quarterly monetary policy decisions. Mr. Mancini-Griffoli spent prior years in the private sector, at Goldman Sachs, the Boston Consulting Group, and technology startups in the Silicon Valley. He holds a PhD from the Graduate Institute in Geneva, and other degrees from the London School of Economics and Stanford University.”

Casheq verdict? Certainly appears credentialed. Part of the Stanford alumni network.

What were those startups? He tells us about it here. He was in San Francisco during the dotcom boom, and was lured by the start-up bug. He joined a small startup working on software to make website, which eventually IPOed. But then decided he wanted to get into policymaking which took him to the LSE.

Events

— Donnie Jr. will be coming to Token2049 in Singapore on October 1-2.

— The BoE is holding a two-day conference focused on “Innovation in money and payments” Sept 3 -4

Further reading

— China is quietly preparing yuan stablecoins as 99 percent of supply minted in dollars. (Crypto Slate)

— Crypto exchange Bullish settles $1.15 billion IPO using stablecoins (The Block)

— The Digital Dirham is coming. (Gulf News)

— There was talk about the digital euro being issued on a public blockchain (FT)

— China’s growing focus on stablecoins is less about embracing crypto and more about defending its currency from U.S. dollar dominance, says Dr. Vera Yuen of Hong Kong University's Business School, who argues the shift highlights offshore opportunities but also deep domestic limits (CoinDesk)

— Redollarization and Digital Statecraft: How Stablecoins Are Rewiring Global Power (Izabella Kaminska interviewed by Financial Sense).

— The Live Stream from the Bitcoin Asia event (Aug 27-28) is here. Eric Trump told the conference “there is not a question to me that bitcoin is going to hit a million dollars”.

— How $34tn flowing into stablecoins will boost these three DeFi protocols (DLNews)

— Do stablecoins increase the net demand for US Treasury securities? (OMFIF)